After reading Redpoint’s 2026 Market Update, my first reaction was: the report’s focus isn’t on “AI is going to change the world again.”

That kind of statement now carries little information.

Its most perplexing aspect lies here:

The AI technological revolution is very real, and traditional software valuations have indeed been slashed.

SaaS may not die immediately, but old software companies will undergo an AI transformation akin to a complete rebuild.

Private AI valuations seem crazy, yet Redpoint attempts to prove that, adjusted for growth, they might not be as outrageous as people think.

It sounds contradictory.

And that’s precisely where its greatest value lies.

It’s not a “Long Live AI” hype piece, nor is it a “SaaS is Dead” panic article.

It’s more like an established Silicon Valley VC firm, standing at the 2026 juncture, attempting to answer a more realistic question:

Is the AI startup window truly real?

Redpoint’s answer is roughly: Yes, it is.

But it’s not a gold rush. It’s more like a high-valuation, high-competition, high-velocity meat grinder.

You can enter, but don’t think of it as easy money.

This article will dissect the report according to its original logic.

I won’t translate it page by page, nor will I endorse it.

What we want to see is: why does it first discuss AI infrastructure, then SaaS valuations, then AI-native startups, and then the private market?

And why does it ultimately state its conviction with restraint, while admitting that many things remain unclear?

This thread is quite important.

For easier reading, I’ll first lay out the report’s logic.

The main body will be broken down into 10 questions, followed by a separate summary of Redpoint’s final stance and the practical implications for AI entrepreneurs:

- Is AI infrastructure another Dotcom Bubble?

- Why does Redpoint believe AI’s market imagination already exceeds software spending?

- Why is coding the first domain to be rewritten by AI?

- What exactly is being killed when SaaS valuations are slashed?

- Why do Vertical SaaS, Infrastructure, and Horizontal SaaS have different fates?

- What are Redpoint’s four biggest concerns?

- Why isn’t adding an AI feature enough for old software companies?

- Why is money still pouring into the private AI market?

- Are private AI valuations truly outrageously expensive?

- Why is this a real window, but also a high-speed meat grinder?

Especially for those working on AI products, AI global expansion, SaaS tools, developer tools, and enterprise software, this report offers a very direct reminder:

The opportunity is huge.

The problem is, many people will also die in big opportunities.

I. AI Infrastructure is Expensive, But Not Like a Pure Air Bubble

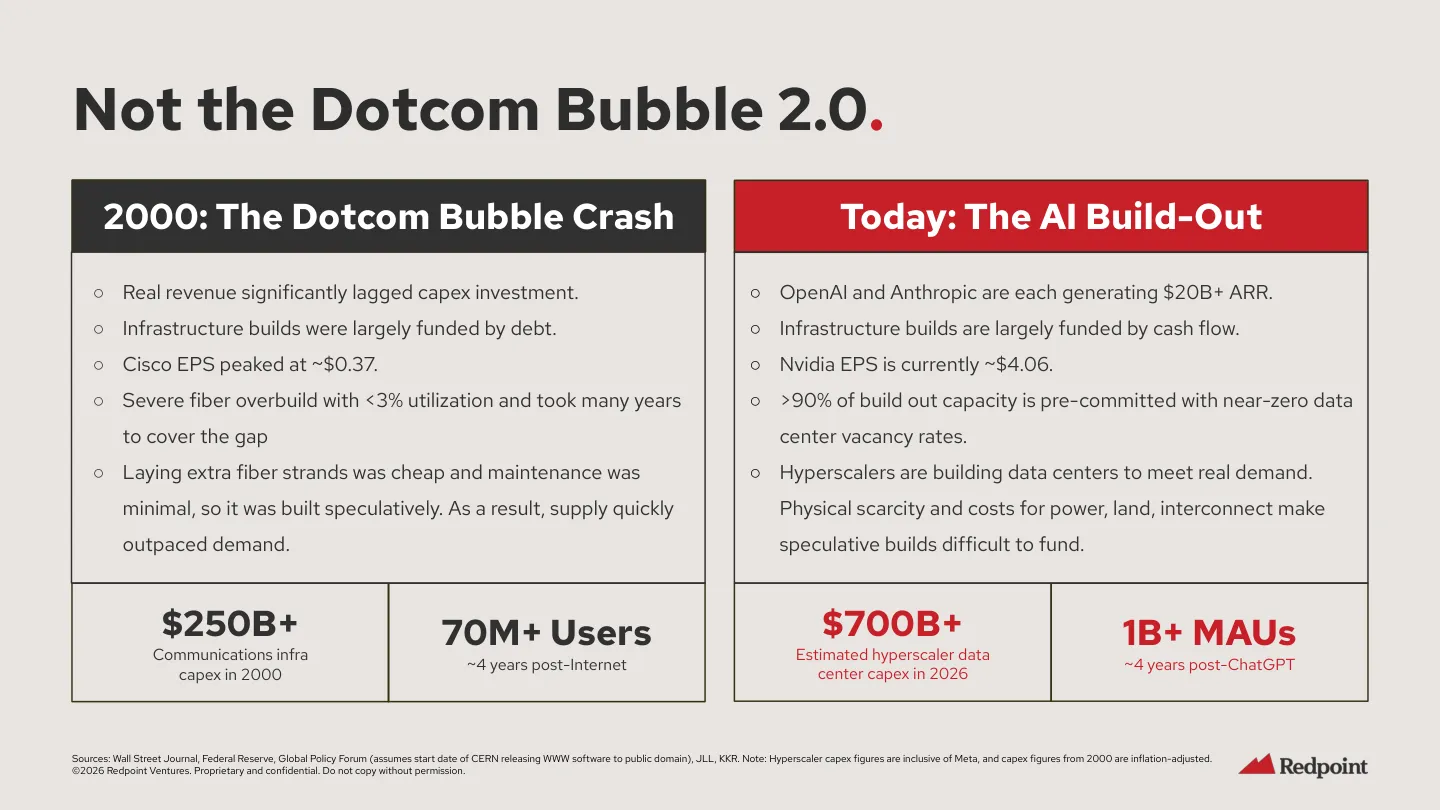

Redpoint immediately addresses a major skepticism: Is AI infrastructure Dotcom Bubble 2.0?

The first few pages of the report compare AI-related capital expenditures to historical tech investment waves.

The message is direct: a technological revolution has indeed arrived, and hyperscalers are pouring real money into data centers, computing power, hardware, and infrastructure.

Redpoint first tempers an oversimplified analogy: don’t rush to equate it with the 2000 internet bubble.

It compares the telecom infrastructure investment of 2000 with today’s AI data center construction.

Back then, telecom infrastructure investment was aggressive, but real revenue significantly lagged, with much construction relying on debt.

The outcome is well-known: fiber oversupply and very low utilization.

Today’s AI build-out is also expensive, perhaps even more so. But the report believes the situation is different.

OpenAI and Anthropic already have high annualized revenues, products like ChatGPT have billions of monthly active users, data center supply is tight, and much capacity is already driven by demand.

This is, of course, Redpoint’s stance.

As a VC, it won’t immediately advise everyone to stop investing and go home.

But its analysis here is still worth examining. It doesn’t say, “True technological revolutions never have bubbles.”

That statement is too foolish; historically, true technological revolutions still had bubbles. It’s more like a reminder: even if this AI wave has a bubble, it’s not entirely made of air.

To put it more bluntly: AI infrastructure is terrifyingly expensive, but at least people are already using the roads. It’s not entirely building highways in the wilderness.

This point is the foundation for all subsequent judgments.

If AI infrastructure were purely speculative, discussing AI software, AI applications, or private AI valuations would be meaningless.

But once there’s real demand behind the infrastructure, the question changes: who will ultimately benefit from this demand?

Old software companies?

AI-native startups?

Infrastructure companies?

Or model companies?

The subsequent sections of the report revolve around this question.

II. Agents Are Still Early, But Valuation Metrics Have Shifted from Software Spend to Payroll

Then it moves to the second layer: AI products are progressing too fast, but Agents haven’t reached full autonomy.

The report lists many product events from 2025 to 2026.

DeepSeek R1, Claude Code, ChatGPT Deep Research, Manus, Vibe Coding, Google AI Search, Sora, Gemini, new Claude versions, Waymo autonomous driving mileage.

These are all placed within this narrative.

Many names, and a very dense pace.

Just listing these names is pointless. We’re already numb from daily news feeds.

Redpoint’s point is: the density of AI product progress is already beginning to change the market’s imagination of software.

Especially the Agent trajectory, which divides maturity into several stages: from Copilot, to Task Agent, to Workflow Agent, and then to Autonomous agents capable of independently performing complex knowledge work.

The report judges that we are largely still in the early stages.

This point must first be established.

Because many articles now discuss Agents as if everyone in the company can go home tomorrow, and enterprise systems will grow legs and do the work themselves.

Redpoint doesn’t say that.

Instead, it clearly tells you that we haven’t reached full autonomy; currently, it’s more about assistance and task execution measured in seconds, minutes, or hours.

But it simultaneously expands the TAM.

In the past, the software market primarily looked at software spending. With AI Agents, Redpoint begins to look at service automation, operational payroll, and knowledge worker salaries.

VCs’ view of AI applications has shifted from “selling a bit more software subscriptions” to “leveraging corporate labor budgets.”

If you still view AI applications through the lens of traditional SaaS, you’ll find many companies outrageously expensive.

A product with little revenue yet, its valuation has already skyrocketed. You’d curse, “Are they crazy?”

If investors are thinking: this thing will eventually consume parts of workflows, parts of service delivery, parts of human roles, then the valuation framework changes.

Of course, even with a changed framework, implementation remains difficult.

So, a repeated reminder follows: a large TAM is just a ticket, not victory.

III. Coding is the First Domino: More Software, Not Simply Fewer Programmers

Next, the report states that coding is the first domino to fall.

This section can easily be misinterpreted as “programmers are doomed.” But Redpoint’s expression is more nuanced.

It asks: why did AI first break through in coding?

Because code can be quickly verified, training data is extremely rich, and output has a clear syntactic structure.

AI labs themselves are most familiar with engineering problems, and code can, in turn, help develop the next generation of models.

These are all reasonable points.

Code, ultimately, is one of the few types of knowledge work that has massive public corpora, clear feedback mechanisms, and can be rapidly verified by machines. It would be strange if AI didn’t tackle this first.

Redpoint doesn’t then say that software development will disappear. It cites data on website growth, iOS apps, and GitHub code growth to illustrate that software production is exploding.

It also uses the historical analogy of ATMs and bank tellers.

ATMs were once thought to replace many tellers, but by reducing branch operating costs, bank branches actually expanded, and teller employment also grew.

This analogy may not be perfectly precise, but it reminds us of an often-overlooked mechanism:

When the unit cost of something drops significantly, demand may not decrease; it might first explode.

AI coding is similar.

It lowers the barrier to making software, but software engineers may not immediately decrease.

Another possibility is that more non-technical people start building tools, more small teams start shipping products, and more internal enterprise processes become software-driven.

Demands that were previously not worth developing suddenly become worth developing.

This is why I think the question “Will AI replace programmers?” is too crude.

A more accurate question should be:

When software production costs decrease, which types of software will proliferate? Which developers will be amplified? And which people who only write glue code, without product judgment or business understanding, will be squeezed out?

Redpoint doesn’t elaborate to this extent, but its direction points to this meaning.

IV. SaaS Valuations Slashed: The Problem Lies in the Ten-Year Terminal Value

Further on, the report begins to address a more pointed topic: Is commercial software nearing its end?

This part is the first major turning point of the entire report.

Earlier, it discussed how the AI revolution is real and software production will increase, all sounding quite optimistic.

But from page 11 onwards, Redpoint directly presents market panic: SaaS apocalypse, AI is killing B2B SaaS, software stocks are being hammered.

Investors are fleeing to other sectors, and SaaS transaction multiples have fallen to very low levels.

At this point, the report’s tone changes.

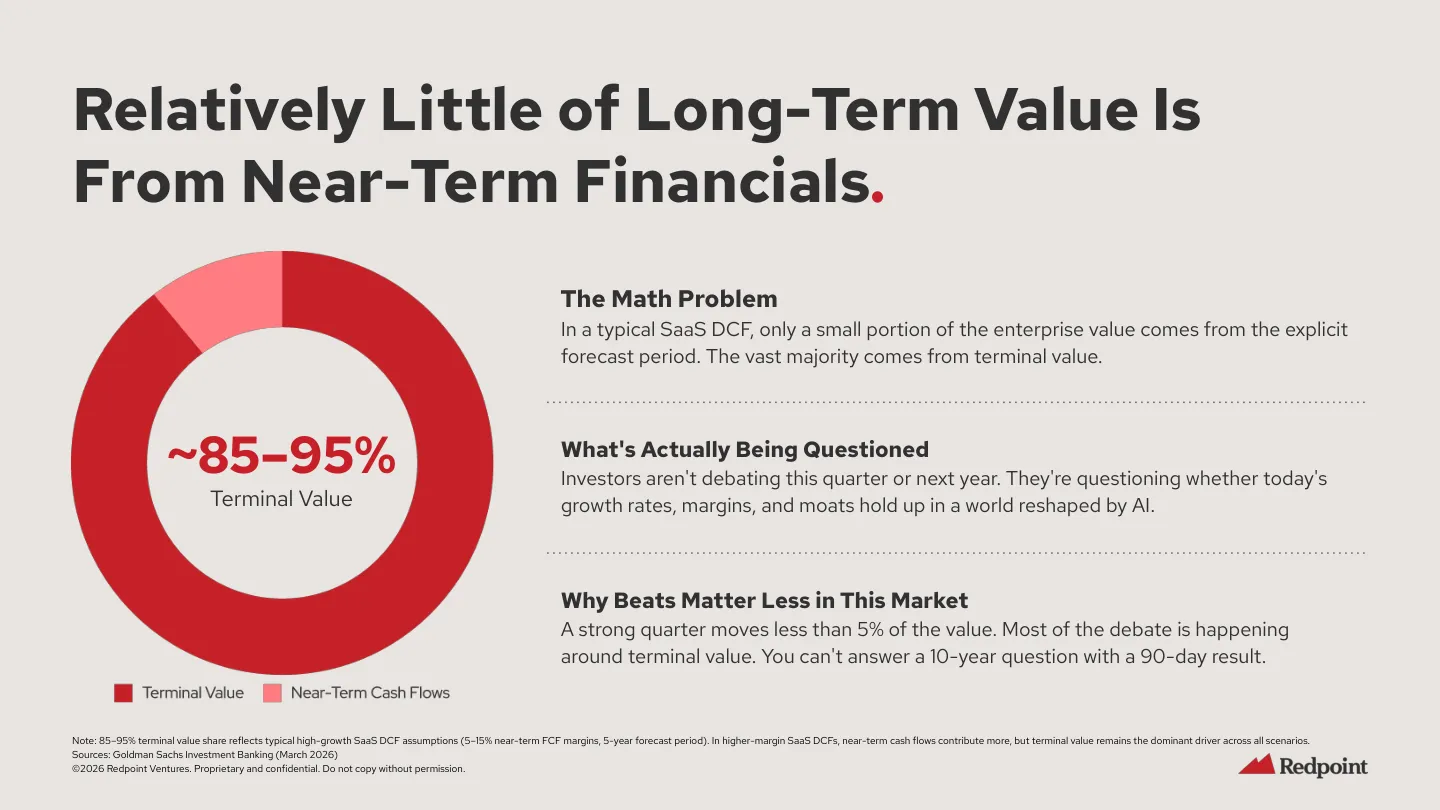

It begins to ask: Has the long-term value of old software companies been repriced?

I think this is the most important part for domestic readers to seriously consider.

Because when we usually talk about AI products, it’s too easy to only look at new things.

Which model got stronger, which Agent can run, which AI coding tool just raised funding, how much monthly revenue a certain app has.

Redpoint’s report is more interesting because it places “new opportunities” and “revaluation of old assets” within the same framework.

Why is the public market killing SaaS?

The reason isn’t that all SaaS companies will collapse next quarter.

The report even specifically states that many software companies’ short-term financials are improving.

The problem is, the public market is starting to doubt their terminal value.

The term terminal value sounds a bit like financial jargon, so I’ll try to explain it more simply.

A large part of a high-growth SaaS company’s valuation doesn’t depend on how much money it can make this year, next year, or the year after.

It relies on the market believing that it can still grow, retain customers, increase prices, and maintain its moat ten years from now.

That’s why Redpoint has a very sharp judgment: you cannot answer a 10-year question with 90-day results.

Good quarterly earnings reports don’t mean the long-term narrative hasn’t already changed.

So many software companies have decent short-term numbers, yet their valuations are cut.

Investors are concerned: after AI enters enterprise workflows, can today’s growth rates, profit margins, retention rates, and moats be sustained for ten years?

There are several layers of pressure here.

First, AI budgets may come from replacing existing software budgets.

Companies won’t suddenly have a huge amount of extra money just for new AI budgets. Often, the money for new AI tools is squeezed from old software budgets.

Second, companies are doing vendor consolidation. CIOs don’t want to add more vendors; instead, they want to reduce them. This is tough for a bunch of point solutions.

Third, seat-based pricing is being challenged.

In the past, SaaS was great because it charged per seat.

With AI, customers will ask: if AI can complete part of a person’s work, why should I still buy so many seats per person?

Can you charge based on usage, results, or workload?

Fourth, the moats of horizontal SaaS are being re-examined.

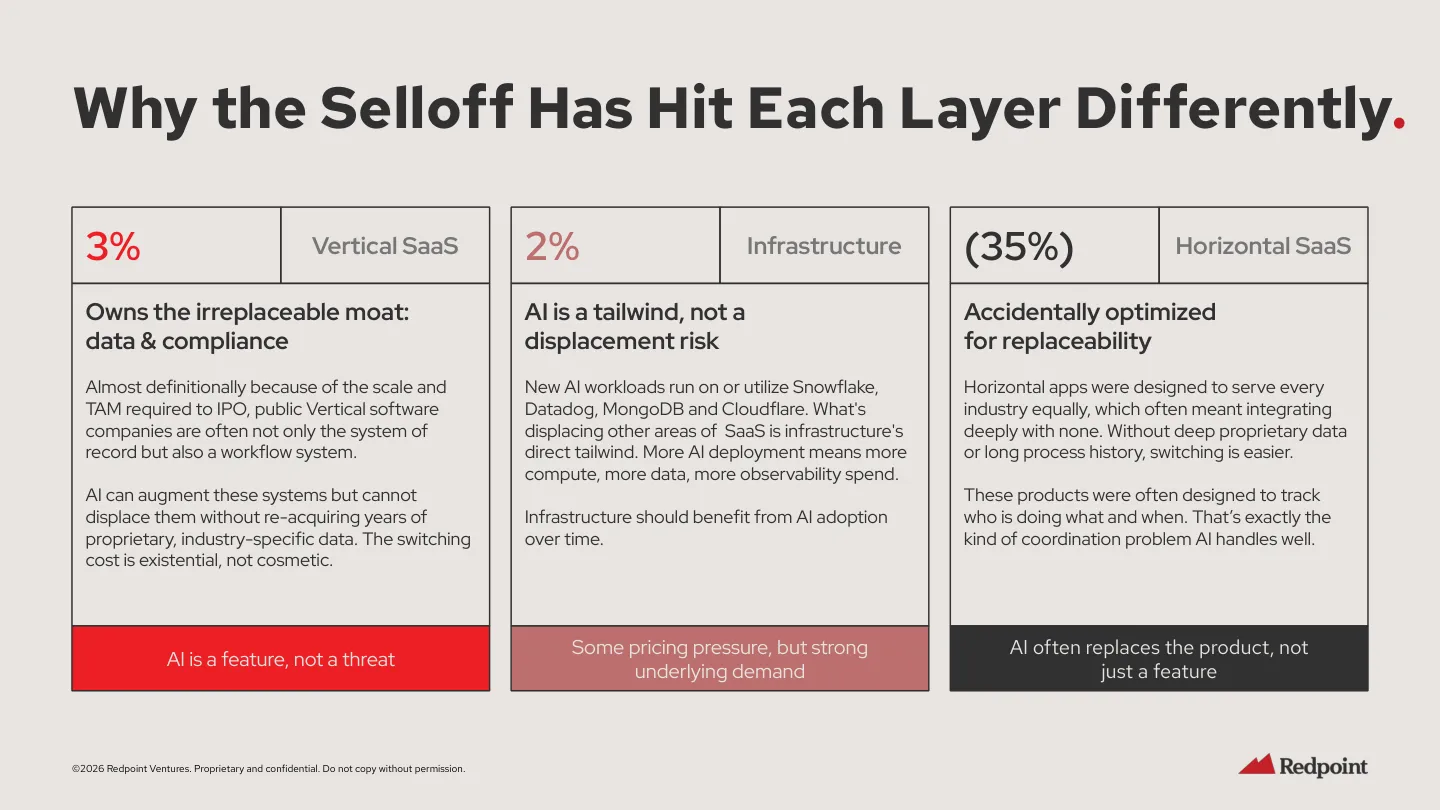

V. The Divergent Fates of Three Software Categories: Vertical, Infra, Horizontal

The report separates Vertical SaaS, Infrastructure, and Horizontal SaaS, which is very interesting.

Vertical SaaS has industry data, compliance, process history, and system records. It will also be impacted by AI, but it still holds a lot of dirty work and industry barriers.

AI is more likely to first become a feature enhancement, not easily replaced directly in the short term.

Infrastructure is more comfortable. The more AI workloads there are, the more data, observability, security, databases, and cloud infrastructure benefit.

You can think of it as: the more others run AI, the more work infrastructure has.

The most awkward is Horizontal SaaS.

The report has a sharp statement, roughly meaning that horizontal SaaS unexpectedly optimized itself into a form that is easier to replace.

Why?

Because to serve all industries, it’s difficult to deeply bind to the data, compliance, and processes of a specific industry.

Its past advantage was generality; today’s risk is also generality.

Many horizontal tools essentially coordinate who does what, when, how to record, and how to report, which is precisely the kind of work AI is very good at re-abstracting.

This statement should not be interpreted as all horizontal SaaS will die.

It illustrates another point: when AI begins to enter enterprises, the market will re-differentiate between “systems of record” and “interface layer tools.”

It will also re-differentiate between “having real workflow data” and “just making tasks look prettier.”

This applies equally to those building AI tools today.

If you’re just building a cheaper, nicer AI wrapper, without data, without workflow depth, without distribution, without customer switching costs.

Then you’re probably not challenging old SaaS.

You’re just replicating the next round of replaceable products.

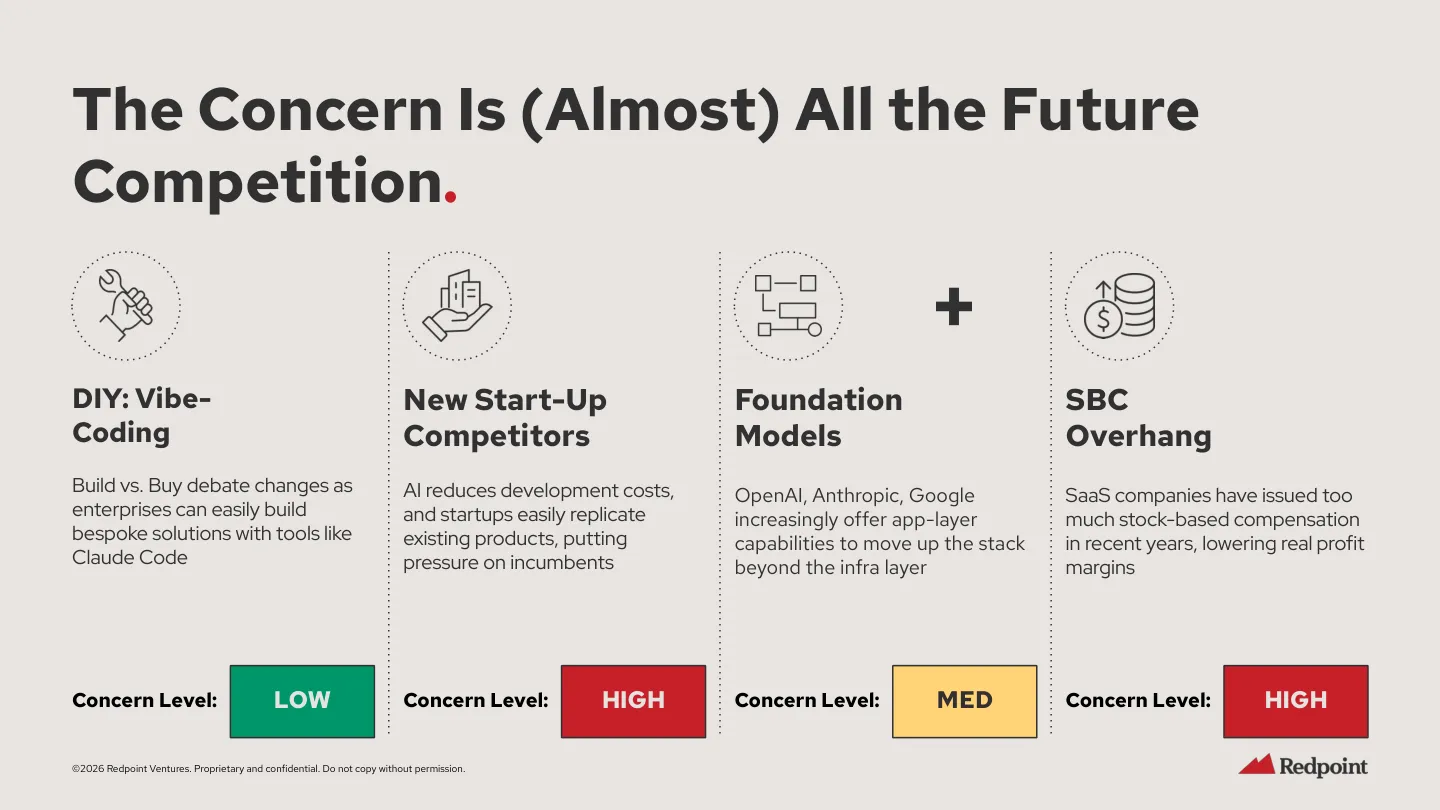

VI. Four Concerns: Enterprise DIY Ranks Lower, New AI Companies and SBC Are More Dangerous

Then the report delves into four specific concerns.

The first concern: DIY / Vibe Coding.

That is, whether companies will use vibe coding to build software themselves.

Redpoint assigns a relatively low level of concern to this.

This might differ from many people’s intuition. Nowadays, everyone talks about Claude Code, Cursor, Lovable, Replit, feeling like anyone can make software, so will companies no longer need to buy SaaS?

The report’s answer is: it’s not that simple.

It uses Slack as an example. When a company buys Slack, it’s not buying just a chat function.

You’re buying mobile access, security, SSO, compliance, stability, monitoring, incident response, continuous updates, zero maintenance, and years of R&D investment behind it.

If you vibe code an internal tool yourself, a demo might be quick. But to have a 1000-person company use it daily, the costs are not in the same league.

I strongly agree with this point.

AI coding can greatly reduce building costs, but it won’t automatically eliminate security, compliance, operations, liability, technical debt, and long-term maintenance.

Many people conflate “making something that runs” with “making a system that an enterprise dares to rely on long-term.”

There’s a lot of dirty work in between.

So Redpoint believes DIY is not the biggest threat.

The second concern: AI-native startups.

This is what Redpoint is more worried about.

The report gives this a high level of concern.

It doesn’t imagine a Fortune 500 company dismantling Salesforce or Workday tomorrow and replacing it with something a young person vibe coded.

More realistic attack vectors are twofold.

One is to layer on top of incumbents, capturing the intelligence layer.

Old systems retain data and contracts, but AI-native startups take the added value of analytics, customer service, intelligent processes, and automated execution.

Customers may not immediately replace systems, but budgets and attention will be drawn to the new intelligence layer.

The other is to target SMBs and the mid-market and move upwards.

Old software is too heavy, expensive, and complex for small customers. AI-native products can use simpler UX, lower prices, and faster delivery to first capture the next generation of customers, then gradually move upmarket.

This is similar to many paths of technological disruption.

Technological disruption usually starts by nibbling at the edges: niche markets, incremental features, new customers, and those whom old systems don’t want to serve.

The third concern: foundation model providers.

That is, whether OpenAI, Anthropic, Google will do everything, directly crushing application layer companies.

Redpoint assigns a medium level of concern.

It acknowledges that model companies are expanding into the application layer, capable of research, coding, multi-step tasks, tool calling, and are also launching various enterprise features.

However, enterprise software still requires domain logic, integration, compliance, UX, collaboration, deployment, and customer success.

This is the last bit of space for application layer entrepreneurs.

Model companies will consume many things, but they may not be willing or adept at completing all the dirty work in every industry.

Applications that survive cannot just be “a shell around a model.” They must encompass the processes, data, compliance, distribution, and delivery within a specific scenario.

The fourth concern: SBC, or stock-based compensation.

This might be less intuitive for many non-financial readers, but it cannot be skipped.

Public software companies historically used stock-based compensation to attract talent, and their financial reports might show decent free cash flow. But once SBC is adjusted for, the true profitability might not be so pretty.

Coupled with AI companies appearing to have higher per-employee efficiency, and traditional software companies continuing to expand headcount, the market naturally re-asks: Is your organizational structure too heavy?

VII. Old Software Companies Need Re-founding; AI Features Are Just Superficial

Redpoint then puts forth a broader judgment: merely adding AI features isn’t enough for old software companies; they need a re-founding.

This section, I believe, is the most relevant part of the report for entrepreneurs.

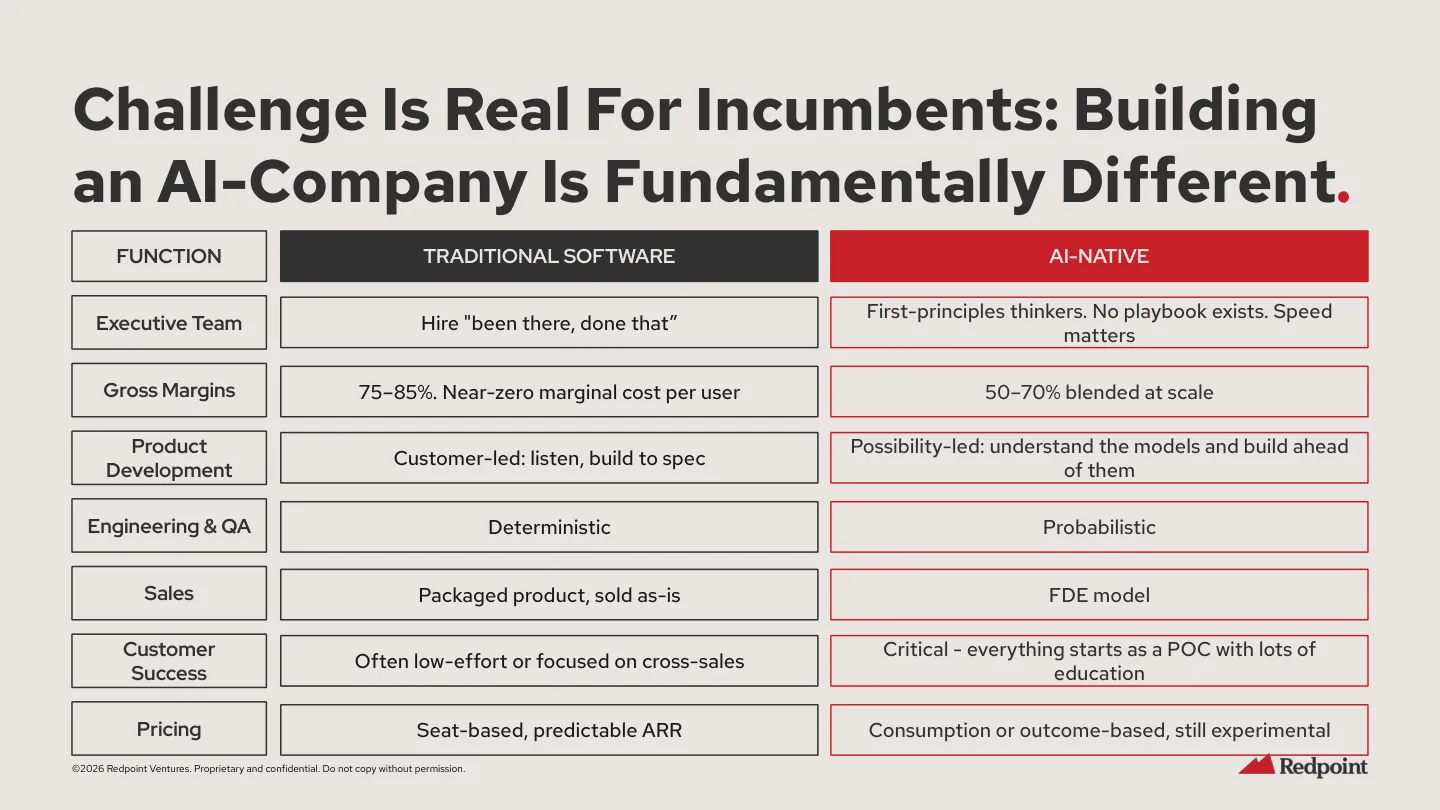

Redpoint compares traditional software companies with AI-native companies.

Traditional software companies prefer to hire “experienced people.” AI-native companies require more first-principles thinking because there’s no existing playbook.

Traditional software has high gross margins, close to zero marginal cost. AI-native companies have real inference costs, so their gross margin structure might be different.

Traditional software product development is more customer-driven. AI-native product development requires a deeper understanding of model capabilities and proactive building.

Traditional software sells packaged products. AI-native might initially be more like an FDE (Field Development Engineer) model, with heavier customer success and education costs.

Traditional software charges per seat. AI-native is more likely to explore usage or outcome-based pricing.

This is no longer minor tweaking.

If you’re just adding a chat box to an old product and calling it an AI Copilot, it’s likely just a transitional product.

Redpoint says that AI’s impact on software companies is akin to an architectural migration. Similar to moving from on-premise to cloud, but potentially at a faster pace.

Companies need to re-examine core product assumptions, data assets, pricing models, and the future product form as model capabilities improve.

This statement is well-suited for tempering expectations.

Many companies’ so-called AI transformation is actually “sticking an intelligent input box next to the original product.”

But if the delivery method, cost structure, sales approach, customer success approach, and pricing model all change, then it’s not a feature update.

It’s a company rebuild.

And company rebuilding is never fun.

For old software companies, it requires organizational courage.

Because you have to admit that existing businesses might not be as valuable anymore, and you have to allow teams to shift from “what customers want, I build” to “what new workflows can models enable.”

You also have to admit that past gross margins, past seat logic, and past sales strategies might all need to be renegotiated.

For startups, it’s not easy either. You can’t just say old companies are slow; you also have to prove you can handle the dirty work.

Enterprise software ultimately isn’t about the demo.

It’s about integration, compliance, stability, ROI, sales cycles, and internal customer politics.

This brings us back to the main theme of our article.

The AI startup window is real, but it’s not a gold rush.

Because you’re not facing a purely new demand market. High expectations, high valuations, high competition, and high delivery complexity will all converge.

VIII. Private AI Opportunities: Applications, Infrastructure, Model Labs

The latter half of the report begins to discuss the private market.

Redpoint believes AI has brought opportunities to the private market. VC funding is rebounding, and AI is driving a large number of new deals.

The late-stage private market has, to some extent, become the new public market.

But money isn’t being spread evenly.

Large sums are increasingly concentrated in a few deals, and companies are reaching ultra-high valuations at an accelerating pace.

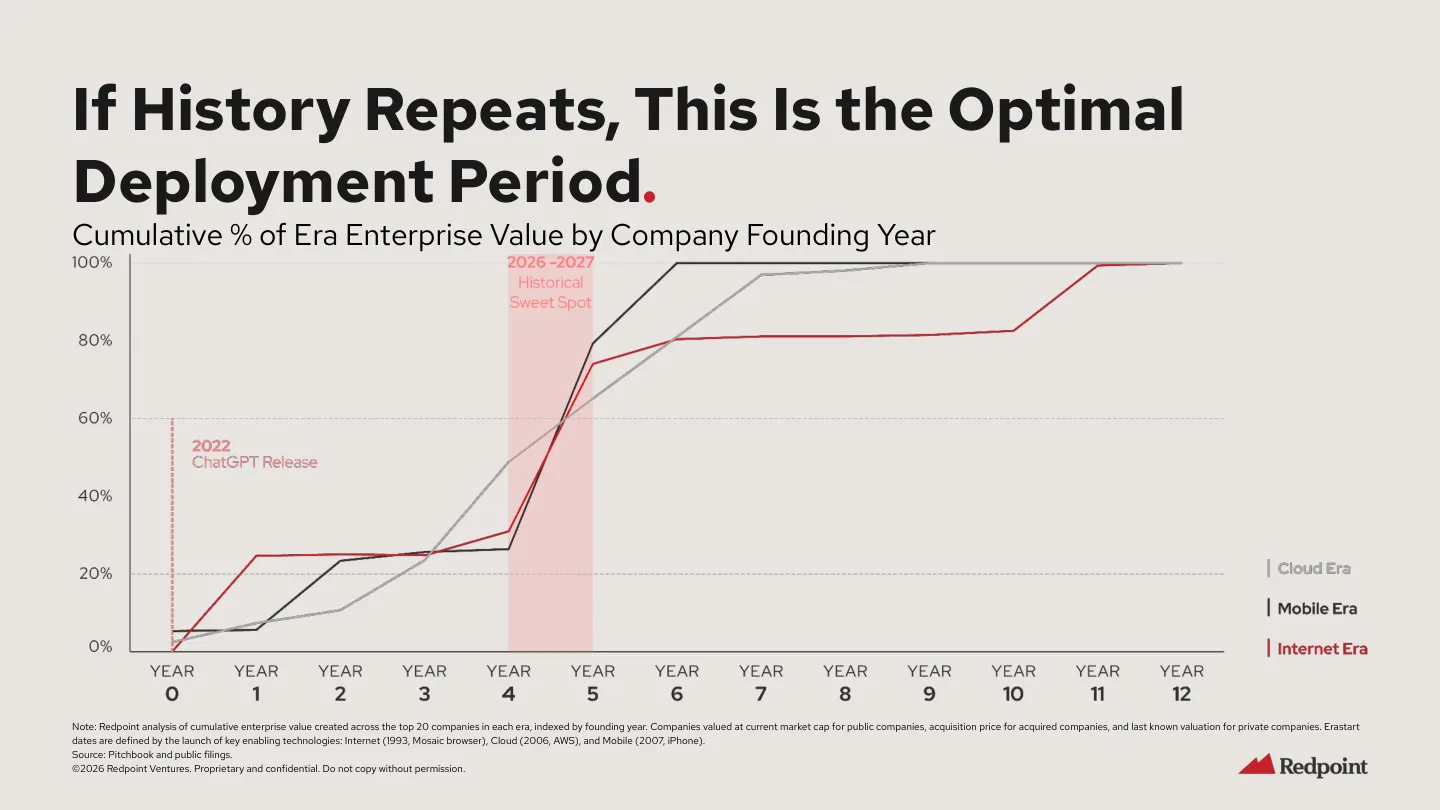

There’s a clear VC narrative here: platform migrations like the internet, cloud, and mobile all gave birth to giants.

So, the 4th to 5th year after ChatGPT could also be the window for durable winners to emerge.

That’s why they say, now is the optimal deployment period.

Translated into plain language: now might be the time to place bets.

But note, it doesn’t say it’s suitable for ordinary people to blindly start businesses.

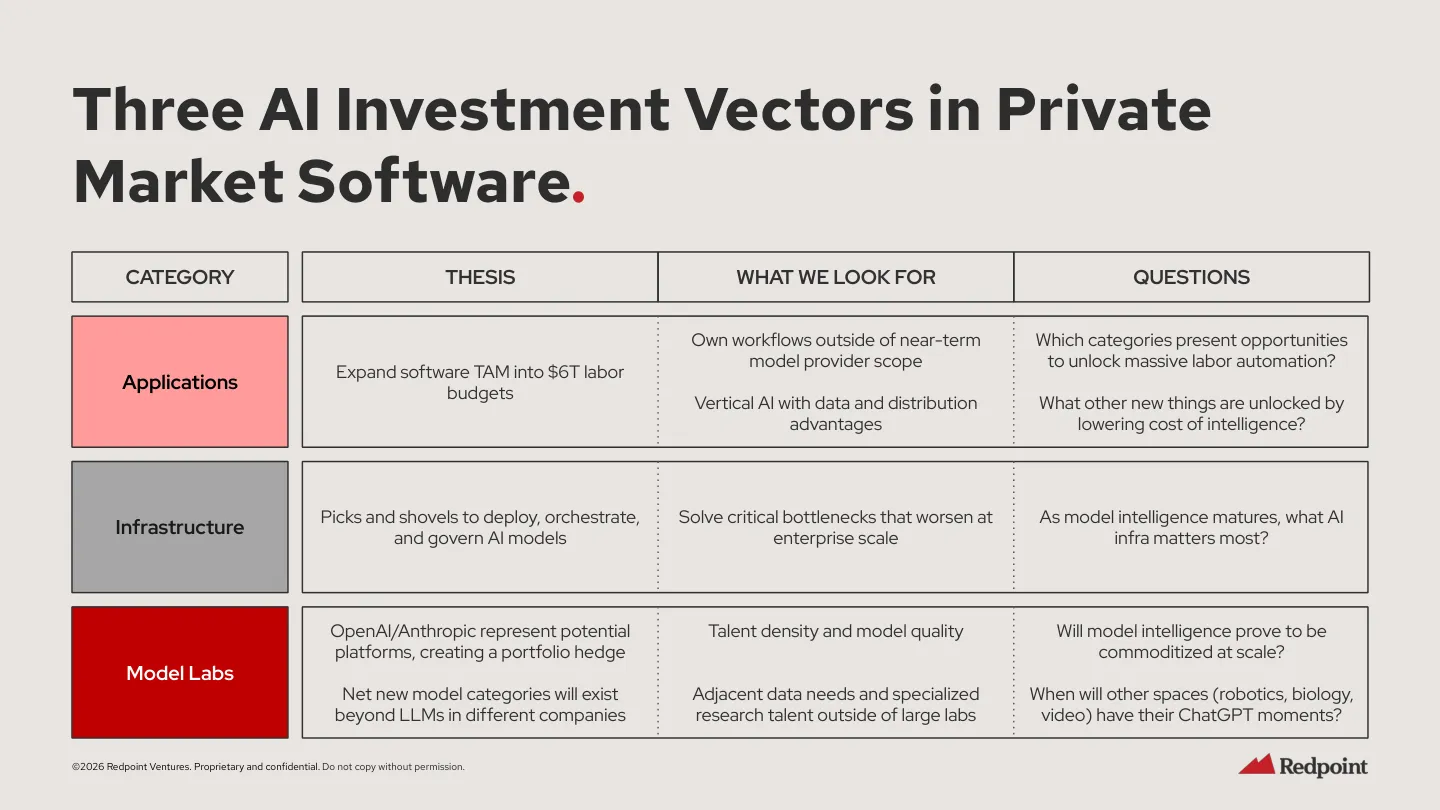

Redpoint divides private AI software opportunities into three categories: applications, infrastructure, and model labs.

The logic for the application layer is to expand the software TAM to labor budgets, capturing real workflows. For example, customer service, legal, clinical documentation, GTM, ITSM, coding, finance, vertical industries.

The application layer is closer to users and revenue. Many AI applications are reaching $100M ARR much faster than in the past, with incredibly high per-person efficiency.

The logic for the infrastructure layer is to solve new bottlenecks that emerge as AI scales within enterprises.

For example, agent security, governance, monitoring, RL loops, orchestration, inference, autonomous testing.

These opportunities currently seem less “sexy” than the application layer. But once agents enter complex enterprise processes, bottlenecks will inevitably appear.

The logic for the model layer is simpler, and more brutal: companies like OpenAI and Anthropic control the intelligence layer and could become new platforms.

At the same time, various new model labs, research spin-outs, and specialized model bets in non-LLM directions will continue to emerge.

But there’s also a contradiction here.

Application layer deals are numerous, but the greatest value might be captured by the model layer.

The infrastructure layer has opportunities, but it needs to wait for real scaling bottlenecks to appear.

The model layer is a generational opportunity, but it requires extremely high talent density, capital density, and research capabilities, making it largely inaccessible to ordinary entrepreneurs.

So, if you are an ordinary AI entrepreneur, don’t stop at the question “Are there still opportunities for AI applications?”

Of course there are.

The more pertinent questions are:

Which layer are you in? Which type of budget are you targeting? Do you have data and distribution? Are you solving a real workflow, or are you building a small feature that could easily be swallowed up after a model upgrade?

IX. Private Valuation Debate: Looks Crazy, But Not So Simple After Growth Adjustment

Next, Redpoint discusses a very controversial point: Are private AI valuations too expensive?

It admits that, if directly compared by revenue multiple, private Series B/C software companies appear outrageously more expensive than public high-growth software.

The report’s YTD 2026 comparison is exaggerated, with private ARR multiples far exceeding public high-growth software companies.

Redpoint then uses growth-adjusted multiple to explain: when growth rate is taken into account, private valuations are not as crazy as they appear on the surface.

Does this calculation make sense?

A little bit.

High-growth companies cannot be rigidly compared to mature public companies solely by revenue multiples. Otherwise, many early-stage investments would always seem absurd.

But this calculation cannot be accepted wholesale either.

Because whether growth rates can be sustained, whether customer retention can be stabilized, whether gross margins can be restored.

Whether model costs will change, whether competition will drive prices down, whether customers will pull back budgets.

These questions cannot be solved by a growth-adjusted multiple.

This is where VC reports are most interesting.

They have logic, and they have a stance.

They need to explain why it’s still worth investing now, so they emphasize the reasonableness after growth adjustment.

When we read it, we shouldn’t blindly get excited, nor should we dismiss it with a simple “it’s all a bubble.”

A better way to read it is: acknowledge that its investment framework offers insights, and also acknowledge that it’s telling an investable story for the market it operates in.

X. The Most Crucial Reminder: The Window is Real, But So is the Difficulty

Then the report itself doesn’t remain optimistic throughout.

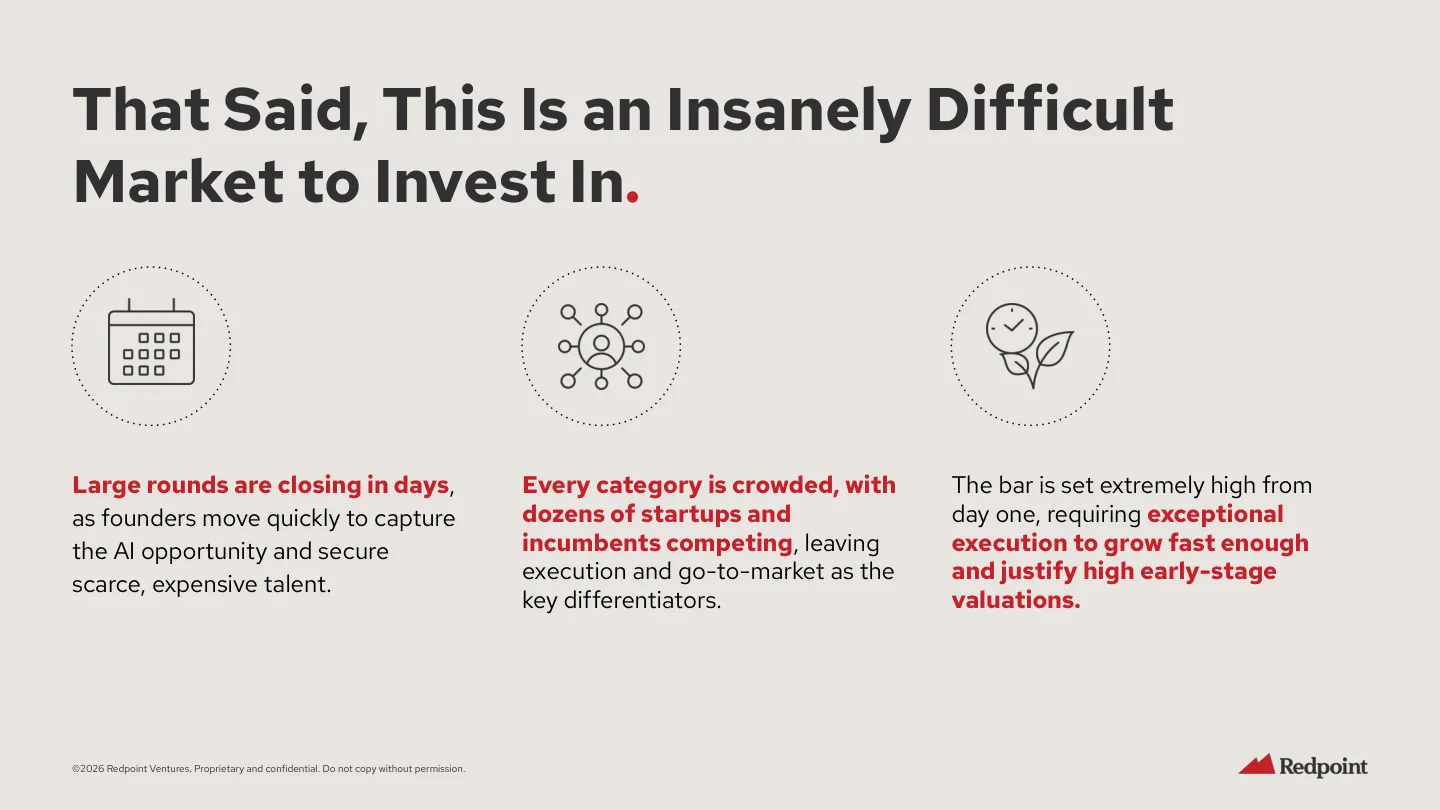

It states very clearly that this is an insanely difficult market to invest in.

Large funding rounds close in days, because founders need to quickly seize opportunities and also compete for scarce, expensive talent.

Valuations are high from day one, and growth expectations are also high from day one. Every interesting category has a bunch of startups, plus a bunch of incumbents stirring things up.

The ultimate differentiation will increasingly come down to execution and go-to-market.

I think this judgment is particularly crucial.

Because many people, upon hearing “AI startup window,” automatically imagine “many opportunities, easy funding, rapid growth, rush in.”

But Redpoint’s latter half is saying something else:

The window is real, but the difficulty is also real.

Fast funding only means people are making more expensive bets in less time.

High valuations might just mean you’re burdened with higher growth pressure from day one.

Lots of competition doesn’t mean the market is big enough for everyone to eat.

Often, it’s the opposite: the more interesting a category, the more dozens of companies rush in together. A few ultimately capture most of the value, while the rest are merely responsible for educating the market.

That’s why I like the term “meat grinder.”

It’s not elegant, but it’s accurate.

AI entrepreneurship has opportunities, but those opportunities are churned together with speed, capital, talent, model iteration, customer budgets, and market narratives.

You just made a demo today, and tomorrow the model company might release a new feature.

You just acquired a few customers, and the day after, ten companies in the same category raise funding.

You just raised your valuation, and the next round of investors will demand you prove you deserve that valuation at an even faster pace.

The difficulty is not ordinary.

It’s high-speed difficulty.

XI. Redpoint’s Final Stance: Conviction, But Not Pretending Omniscience

Finally, Redpoint still offers an optimistic but restrained conclusion.

Redpoint refers to the $6T labor budget as arithmetic.

Not a visionary slogan, but a market size they calculated based on the US professional labor wage pool.

Even if AI only penetrates a small portion of the professional labor market, it could exceed the existing software market.

It also believes that the 4th to 5th year after a platform migration is often the window when durable winners begin to emerge.

ChatGPT was released in November 2022, so by 2026, it indeed falls within this timeframe.

Looking further at the application layer, previous platform migrations have not eliminated application layer opportunities. While the underlying infrastructure changes, new companies will still grow in the application layer.

But it also admits that many things remain unclear.

Which software categories will be compressed fastest, is unclear.

Which old software companies can successfully undergo AI transformation, is unclear.

When the public market will re-rate, is unclear.

Where OpenAI, Anthropic, Google, and other model companies will expand next, is unclear.

This is one of the more honest aspects of the report.

It doesn’t say, “We know who the winners are.” It only says that AI will reallocate value in the software industry. As for who wins specifically, how they win, and when they win, it remains chaotic.

XII. Practical Reminders for AI Entrepreneurs

So, if I were to summarize this report in one sentence, I wouldn’t just say, “Redpoint is bullish on AI.”

That’s too shallow.

I would say:

Redpoint believes that AI has ushered the software industry into a new window.

This window won’t hand out money to everyone; it will use higher valuations, faster speeds, and greater competitive intensity to filter out those who can translate AI into workflows, revenue, and organizational efficiency.

For domestic AI entrepreneurs, independent developers, and global expansion teams, here are a few practical reminders.

First, don’t just focus on “can it be built?”

AI coding makes products easier, but enterprise software often gets stuck not at the demo stage.

It gets stuck at data, compliance, integration, distribution, stability, and whether customers are willing to switch.

Second, don’t just build horizontal small features.

If your product lacks data depth, process depth, or real scenarios for a specific type of customer, and is merely “model + UI + prompts.”

Then you might also become what Redpoint calls “optimized for replaceability.”

Third, don’t mistake high valuations for market validation.

Fast funding and high valuations in the AI sector often mean you need to run even faster. A high valuation is not a shield; it’s more like a countdown timer.

Fourth, don’t blindly believe in model companies, nor underestimate them.

They will consume many general capabilities, but there’s still a lot of dirty work in enterprise software.

The opportunity in the application layer lies in your willingness to tackle this dirty work, not just waiting for models to get stronger.

Fifth, don’t interpret “AI transformation” as adding a chat box.

If your workflow, pricing, gross margin, delivery, customer success, and organizational methods haven’t changed, then you’re likely just slapping an AI label on an old product.

This stage might sell for a while, but it might not withstand the next round of revaluation.

Conclusion: The Wind Will Come In, And So Will the Blades

Writing this, I feel that the value of this report lies not in giving us a definitive answer.

It offers a kind of clear-headed excitement.

The AI startup window is real.

Redpoint, as a VC, naturally hopes this window is real and naturally wants to tell an investable story. But it didn’t paint this story as a gold rush.

It speaks of capital becoming more concentrated, rounds becoming faster, valuations becoming higher, and competition becoming denser.

The application layer has revenue, infrastructure has bottlenecks, the model layer has platform opportunities, old software companies face transformation pressure, and the public market has terminal value doubts.

This is more useful than simple optimism.

Because those entering the arena are not most afraid of not knowing there’s an opportunity.

They are most afraid of only seeing the opportunity, without seeing the cost.

When the window opens, the wind will come in.

And so will the blades.

The AI startup game has long surpassed “who can build something.”

It’s now more like: who can truly tackle a real problem when capital, models, customers, distribution, delivery, and organizational speed are all simultaneously pressing down.

This is what makes Redpoint’s 2026 Market Update report most worth dissecting.

The question is no longer whether AI will change the world.

The question has become: when the world truly begins to change, who can survive this meat grinder?